As old as the world is, fraud holds its position and causes huge problems for business owners and all persons involved if detected. In 2010 a medium estimated loss due to fraud for businesses was 5% annually. In 2018, it was the same — even though we don't know the results of the 2019th report yet, there is no chance for better results.

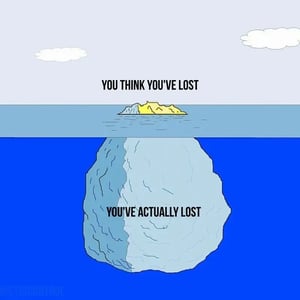

We understand fraud as intentional deceit for profit or advantage - a harmful deed we would condemn being an injured party. That's a thing everybody knows more or less, but not anybody knows about the reasons for fraud and its consequences. The iceberg of fraud is very helpful in depicting information that is left unreported. While 5% of financial losses is a number we know about, how many fraudulent operations are concealed? We can't say, but we can dive into more accessible facts on fraudsters and their motives.

Geometry of fraud

Fraud and its techniques are evolving, and so does a scientific approach to fraud and explanations of it. There is no one general explanation of fraud or a fit-all solution, but there are some popular and known researches that belong to fraud classic. Is fraud a triangle or square?

The fraud triangle is a scheme of fraud motives that includes pressure, opportunity, and rationalization. A triangle was developed a long time ago (in 1953, to be precise) by Donald Cressey - it's still relevant and was supplemented by other scholars. The pressure is simply a lack of finances or other resources for living. It also can be work-related (the work itself isn't satisfying, or the salary is below the minimum level).

More straightforward in the triangle is the opportunity - everything you haven't done for your company for its safety will work against you. Fraudsters use opportunities such as delayed audits, security breaches, absence of performance quality evaluation, and many others. Finally, a rationalization - an excuse to steal because the company owes you because it wasn't a large sum of many because everyone in your position would do the same.

Only three components of fraud seem to be too general - that's why we know about the square (or diamond) of fraud, fraud pentagon, and more complicated models. The fraud square is very similar to the triangle with its incentive, opportunity, and realization. But it has one crucial detail - a fraudster should have certain capabilities to commit fraud or conceal it for a long time.

A variety of fraud schemes is understandable: potential fraudsters may have a motive, but don't have an opportunity, or have an opportunity but are not smart enough to create any fraud schemes. Still, all fraudsters generally share living beyond means, desires for personal gain, and even revenge motives - things that are not so easy to detect.

Talented and dangerous

Now let's get back to the capabilities that fraudsters should have. A decent mental capacity is a must for fraudsters - 47% of perpetrators have a university degree, and 14% are postgraduates. The more educated the fraudsters are, the larger sum of their fraud will be - postgraduates are more likely to engage in complicated schemes of fraud.

Smart and cunning, fraudsters analyze accounting and internal control systems, are aware of tax evasion schemes, know the weaknesses of their victims, and manipulate facts and shreds of evidence. It's not uncommon when fraudsters provide auditors with false evidence or point at a smaller case of fraud to conceal a big one. To detect a fraudster, you need to evaluate him without any prejudice and not under his influence - that's why external audits may work better than internal inspections.

Age, gender, status, loyalty

Along with high intelligence, four more factors characterize a fraudster. Belonging to a specific age group is important - statistics place perpetrators between 30-50 years old. Too young employees usually have no knowledge about all the processes in the company and don't take high positions. In contrast, older employees are capable of fraud but value their jobs and don't take risks.

Talking about status, we mean position in the company - social status doesn't affect the probability of fraud. The highest proportion of fraud share managers and employees, both groups, take up to 40%. It's rare for owners and executives to take part in the fraudulent operation; though, when they do, losses are way more significant.

We've already discussed which role gender plays in corruption, and it's not so different in terms of fraud. The majority of fraudsters are male: they take more high positions in the company and have lower ethical sensitivity, compared to women. The more gender-diverse the company board is, the lower risk of corruption it will have - a simple solution for protecting your interests.

What's with loyalty? Loyal workers with a competitive salary and a good reputation in the company will obviously be less likely to commit fraud. However, remember about red flags: when an employee takes full control over one activity, doesn't delegate tasks he is not responsible for, behaves isolated from others, or never takes days off - what does he cover up?

Everything is under control

Fraud occurs when there are internal breaches in the company no one took care of. Corporate culture, established systems of control of finances, and a code of conduct - all are essential in creating a non-fraud environment. A company is a small version of the society where you live - in many aspects, it determines the behavior of the employee. Excellent work results and high performance should be encouraged, while for fraudulent actions, there should be a serious punishment all employees know about.

Step by step, the company builds its approach to fraud and forms structures that make fraud perpetration impossible. A real hierarchy of positions should be a positive addition: when managers control the staff, someone should control managers. Whistleblower hotlines and external companies may help supervise your business.

A safe and reliable work environment starts from details - it is easier to prevent fraud than investigate it. That's why fraudsters should be stopped on the way to your company - hire the right people and ensure that all the employees are carefully selected. An interesting fact: fraudsters don't show any psychological deviation and aren't any different from their colleagues. Don't let an honest person become a fraudster - you've hired the right employee, so treat him well.

Quuuuiz time!

The annual median loss caused by fraud takes up to $7.1 billion - can you imagine? Since it's cheaper to misdiagnose a standard transaction as a fraudulent one than miss fraud at all, we sincerely recommend you to be alert. Fraudsters will not miss their chances to fool you - are you ready to catch them?